Executive Summary

Zepto, a pioneer in India’s quick commerce sector, has filed its Draft Red Herring Prospectus (DRHP) for an upcoming Initial Public Offering (IPO). Analysis of the filing reveals a company in a state of hyper-growth, with revenue for FY 2026 reaching ₹22,623 crore. However, the path to profitability remains challenging, as evidenced by a net loss of ₹5,905 crore in the same period. While Zepto has successfully reduced fixed costs and digital marketing expenses per order, it faces significant headwinds in supply chain variable costs and high attrition rates among its operating staff.

Company Overview

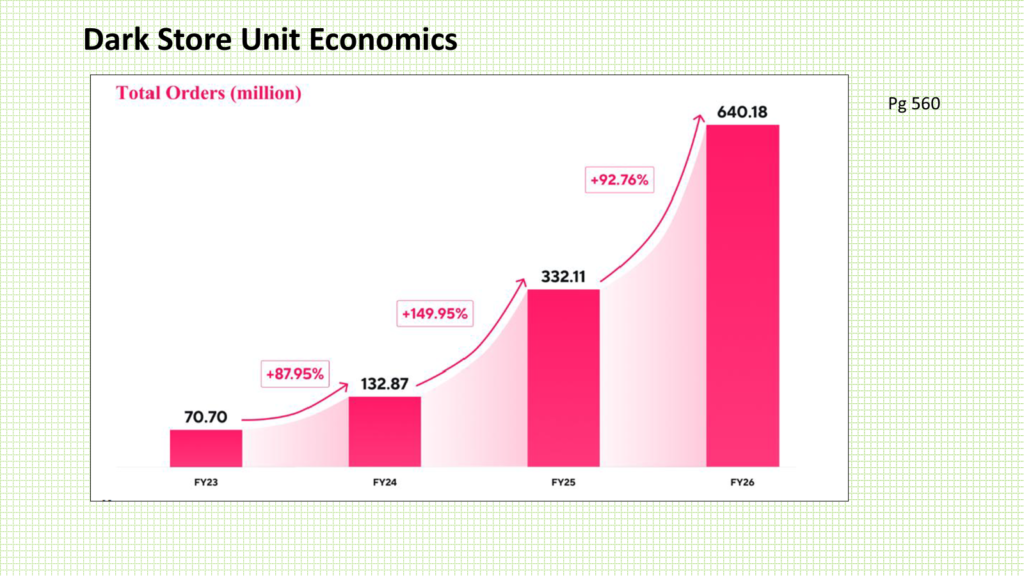

Zepto operates in the competitive quick commerce space, promising ultra-fast delivery of groceries and household essentials. The company has seen a meteoric rise in order volume, growing from 70 million orders in FY 2023 to 640 million orders in FY 2026. As it prepares to go public, the focus shifts from pure growth to the sustainability of its business model and its ability to achieve positive unit economics.

Business Model

Zepto’s primary model involves purchasing goods from merchants and selling them through a network of “dark stores”—micro-warehouses situated close to high-demand residential areas. The company utilizes a densification strategy. This strategy creates a flywheel effect: higher order density leads to more dark stores, which reduces the average delivery distance per order, thereby increasing efficiency and user value.

Revenue Analysis

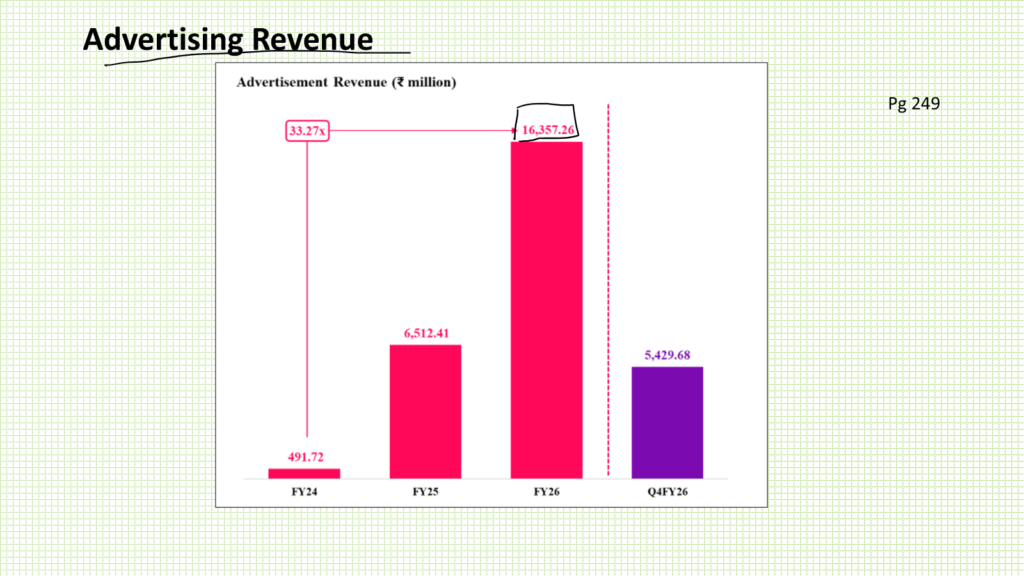

Zepto’s revenue from operations stood at ₹22,623 crore in FY 2026. A significant and growing contributor to the top line is advertisement revenue. Ad revenue grew 33-fold from FY 2024 to FY 2026, reaching approximately ₹1,635.7 crore, which accounts for roughly 7% of total revenue. In the fourth quarter of FY 2026 alone, the company generated ₹542 crore from ads, highlighting its strength as a high-traffic digital platform.

Cost Structure

A granular look at Zepto’s expenses reveals that its core operating costs exceed its total revenue:

- Cost of Goods Sold (COGS): At ₹18,198 crore, purchasing traded goods consumes 80% of revenue.

- Delivery and Benefits Expense: This accounts for ₹3,046 crore (13% of revenue), covering delivery drivers and packaging.

- Employee Benefits: Standard salaries and benefits total ₹1,784 crore (7.89% of revenue).

The sum of these three major expenses—COGS, delivery, and employee benefits—is greater than 100% of the company’s total revenue from operations, suggesting that the current model requires significant efficiency gains to reach break-even.

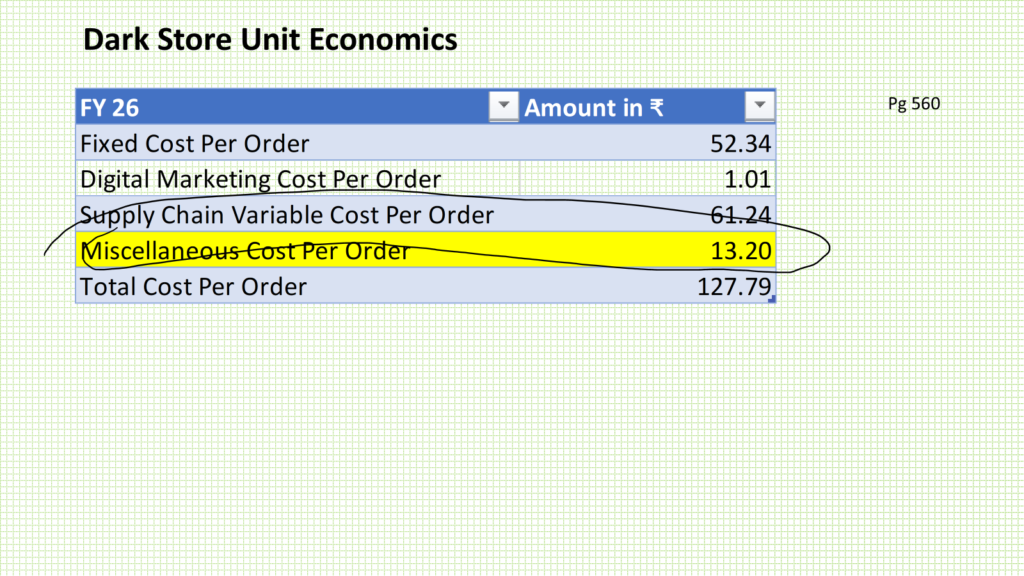

Unit Economics

The company has made notable strides in order-level economics as volumes have increased:

| Metric (Per Order) | June 2023 (3 Mo) | March 2026 (3 Mo) |

|---|---|---|

| Fixed Cost | ₹80 | ₹52 |

| Digital Marketing Cost | ₹10 | ₹1 |

| Adjusted EBITDA | -₹95 | -₹59.40 |

| Supply Chain Variable Cost | ₹63 | ₹61.24 |

While fixed and marketing costs have plummeted due to scale, the supply chain variable cost has only decreased by approximately ₹2 over three years. This suggests a floor for efficiency gains due to the inherent costs of manual labor and last-mile logistics.

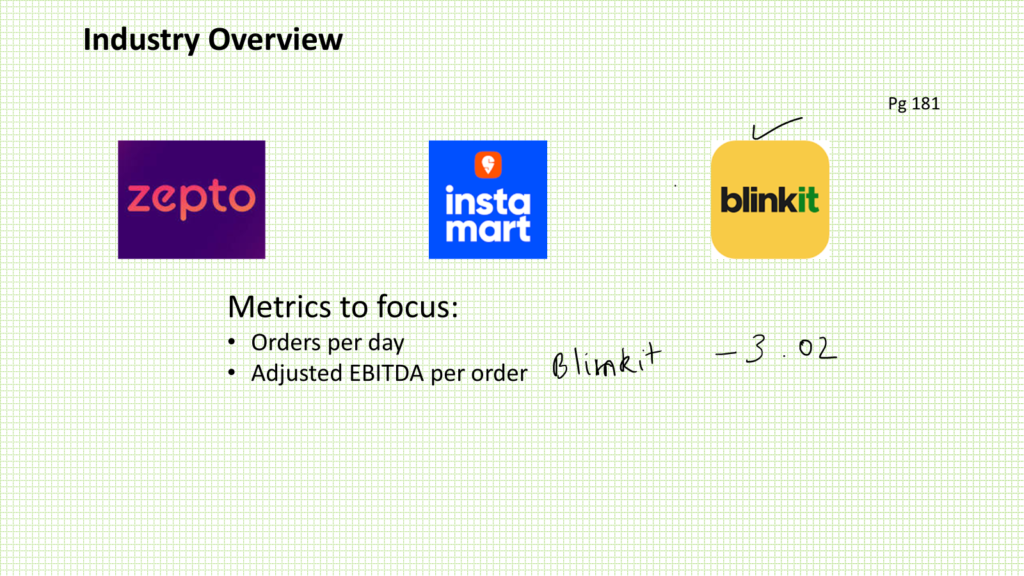

Competitive Landscape

Zepto currently ranks as a major player in the Indian quick commerce market, trailing Blinkit but competing closely with Swiggy Instamart. In FY 2026:

- Blinkit: 916 million orders with an Adjusted EBITDA per order of -₹3.02.

- Zepto: 640 million orders with an Adjusted EBITDA per order of -₹78.75 (on an annualized basis).

- Instamart: 412 million orders with an Adjusted EBITDA per order of -₹85.18.

Strategic Advantages

- Rapid Scalability: Zepto is one of the fastest-growing platforms, doubling its order volume year-over-year.

- Ad Revenue Momentum: The ability to monetize platform traffic through high-margin advertising provides a critical buffer against thin retail margins.

- Order Density: The densification strategy is actively reducing fixed costs per order as the network matures.

Key Risks

- High Labor Attrition: While corporate attrition is 15%, the attrition rate for operating staff stands at 90%. This churn creates constant pressure on recruitment and training costs.

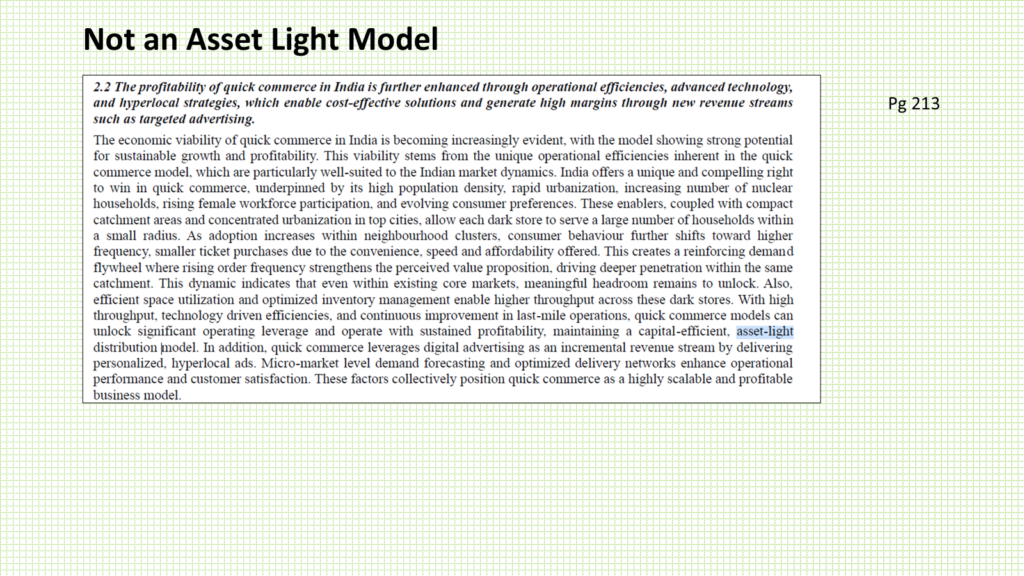

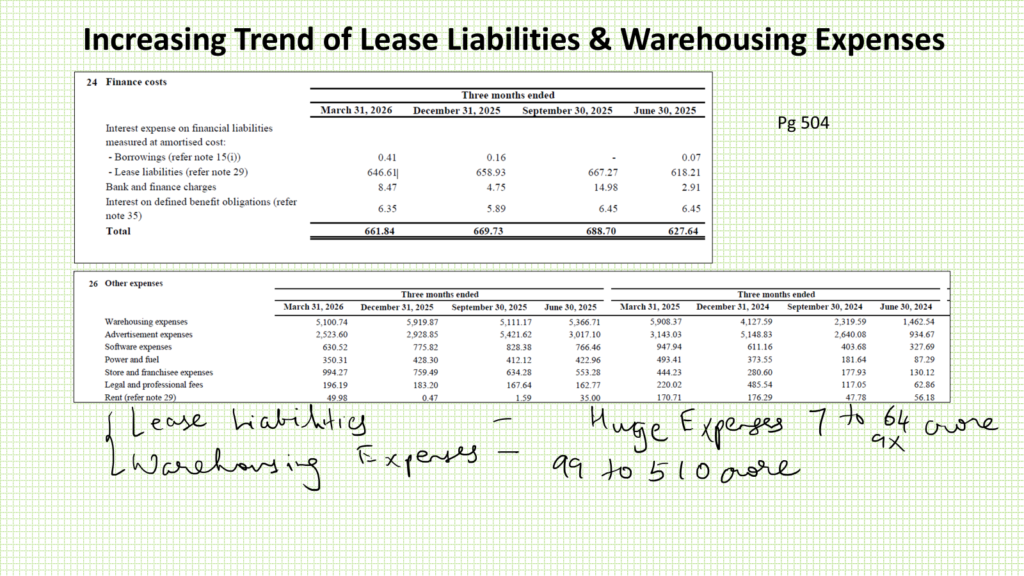

- Rising Lease Liabilities: Despite claiming an “asset-light” model, interest on lease liabilities jumped from ₹7 crore in mid-2023 to ₹64 crore by March 2026.

- Utilization of IPO Proceeds: A portion of the ₹8,010 crore fresh issue is slated for lease rental payments for existing dark stores, which some analysts view as a potential red flag for operational sustainability.

Growth Opportunities

The primary growth opportunity lies in the continued expansion of the dark store network to unlock further operating leverage. Additionally, Zepto has the potential to increase its average order value (AOV) and expand its higher-margin private label or non-grocery categories to offset sticky delivery costs.

Key Takeaways

- Zepto is scaling aggressively, with a massive jump in total orders to 640 million.

- Free Cash Flow (FCF) per order is improving, moving from -₹93 in 2024 to -₹67 in 2026.

- Supply chain variable costs are a persistent bottleneck, showing only marginal improvement despite massive volume increases.

- Existing investors are selling less than 1% of total shares in the Offer for Sale (OFS), indicating continued skin in the game for early backers.

Conclusion

Zepto’s DRHP paints a picture of a company successfully executing a growth-at-all-costs strategy while gradually refining its unit economics. While the explosion in advertising revenue and the reduction in fixed costs per order are positive signs, the high attrition rates and rising lease liabilities remain significant hurdles. For investors, the central question is whether Zepto can achieve the near-breakeven efficiency demonstrated by competitors like Blinkit before its capital reserves are exhausted.